Key takeaways

- Monarch Money is well-designed and has earned its reputation, but at $99.99/year it's the most expensive option in the category and the value proposition is clearest for couples budgeting together, not solo users.

- YNAB's zero-based budgeting philosophy is genuinely effective, but the system requires active weekly maintenance. Users who want passive tracking consistently abandon it within two to three months.

- Rocket Money is an excellent subscription-cancellation tool. As a full budgeting replacement for Mint, it's underpowered, and its pricing structure is deliberately opaque.

- Copilot is the best-designed app in the category by a significant margin, but iOS and Mac exclusivity eliminates it for roughly half the potential audience.

- Most Mint refugees needed five things: automatic bank sync, real spending limits, a clear monthly cash flow view, cross-platform access, and a price under $50/year. No single alternative delivers all five.

- The right choice depends almost entirely on one question: how actively do you want to manage your money? That answer narrows the field immediately.

I want to be upfront about something before we get into this. I've been building Balance Pro, a personal finance app, since 2014. That makes me a direct competitor to every app I'm about to discuss. I have a financial interest in you choosing Balance Pro over the alternatives.

I'm telling you that now because I think it actually makes what follows more useful. I've spent more than a decade watching how people use budgeting apps, what makes them stick, what makes them quit, and what the realistic differences are between tools that all promise to "help you manage your money." I've read through more App Store reviews, Reddit threads, and user feedback sessions than I can count. And since Mint shut down in October 2023, I've had hundreds of conversations with people who were working through the migration, trying each alternative in sequence, and ending up frustrated by the gap between how these apps are marketed and how they actually behave in practice.

When Mint users first started asking me which alternative I recommended, I pointed a lot of them toward Monarch Money. It seemed like the most direct replacement: automatic bank sync, clean interface, real budgeting categories, couples features. After watching enough of those users come back to describe their actual experience, I stopped recommending it as reflexively as I had been. The app isn't bad. The mismatch between what most Mint refugees needed and what Monarch delivers is the issue, and it took enough conversations to see the pattern clearly.

This is that pattern, written out in full. Biases disclosed, competitive interest noted, and as honest as I know how to be.

What actually happened when Mint shut down

Mint had been around since 2006. Intuit acquired it in 2009 for $170 million, which was a remarkable sum for a product that gave away its core service for free. The business model was referrals: Mint would show you your credit card spending and then suggest you apply for a different credit card with better rewards. It would show you your savings account balance and recommend a high-yield alternative. The app made money every time a user clicked through to a financial product and opened an account.

That model held up for over a decade, but by the early 2020s, the economics had deteriorated. Financial product referral rates had compressed, users were getting savvier about ad-supported services, and Mint's infrastructure wasn't cheap. Intuit also owned Credit Karma, which occupied a similar position in the financial data ecosystem with better monetization. In October 2023, Intuit announced it was shutting Mint down and redirecting users to Credit Karma.

Credit Karma is not a budgeting app. It tracks your credit score and shows you targeted offers for credit cards, loans, and insurance. It doesn't have budget categories. It doesn't let you set spending limits. It doesn't give you a monthly cash flow picture. The redirect was, to be direct about it, not an honest replacement for what Mint users had been using.

Mint had approximately 3.6 million active users at the time of the announcement. Many of them had been using the app for years, had their full transaction history in it, and relied on its budgeting categories as a core part of how they managed money. The shutdown gave users a few months to export their data and find an alternative, which was enough time in theory and not enough time in practice for people to properly evaluate their options.

What followed was exactly the kind of rushed decision-making you'd expect from users who'd had their primary financial tool yanked out from under them. Monarch Money ran aggressive acquisition campaigns explicitly targeting Mint refugees. YNAB's existing community recommended it loudly in every forum discussion. Copilot got written up in tech publications. And Rocket Money, which had been quietly building out beyond its subscription-cancellation roots, positioned itself as a simple replacement.

Most of the users I've spoken with tried at least two of these before settling, and a significant number are still not fully satisfied with where they landed. That's the context for this comparison.

What Mint users actually needed

Before evaluating any alternative, it helps to be specific about what Mint actually provided that people valued. The answer isn't "everything Mint did." A lot of Mint's features were underused or actively disliked. The referral-driven credit card recommendations were irritating. The credit score monitoring was duplicated in a dozen other free tools. The mobile app was clunky by modern standards.

What people valued was a specific combination:

- Automatic bank sync. Transactions imported from checking, savings, and credit card accounts without manual entry. Mint connected to nearly every US financial institution through Plaid and similar aggregators, and it mostly worked without requiring re-authentication every few weeks.

- Budget categories with real limits. Not just a ledger of what you spent, but a system that said "you have $300 for restaurants this month" and showed you how much was left. The color change from green to red as you approached the limit was a simple behavioral nudge that genuinely worked for a lot of users.

- A clear monthly income vs. spending view. How much came in, how much went out, how much was left. Not a net worth chart, not a credit score widget, just the basic cash flow question answered clearly.

- Cross-platform availability. iOS, Android, and a browser that worked on any computer. Mint users weren't locked into a single device ecosystem.

- Free. This is the constraint that all the alternatives fail, but it's important to acknowledge that Mint's zero-price point was not arbitrary generosity. It was a business model that no longer worked. The alternatives charge because they have to. But the psychological gap between "free" and "$100 a year" is real, and it affects user behavior.

Against that list, the alternatives each make a different set of tradeoffs. Understanding which tradeoff matters most to you is the actual decision, and the "best Mint alternative" roundups that circulate online typically don't help you figure that out because they don't start from what you specifically needed.

Monarch Money: the most direct replacement, with a price that's hard to defend for most users

Monarch Money launched in 2019, before Mint's shutdown was even a rumor. The timing turned out to be fortunate: when Mint announced it was closing, Monarch was already positioned as a premium alternative with a similar feature set, and it executed a highly effective migration campaign that captured a large share of the displaced users.

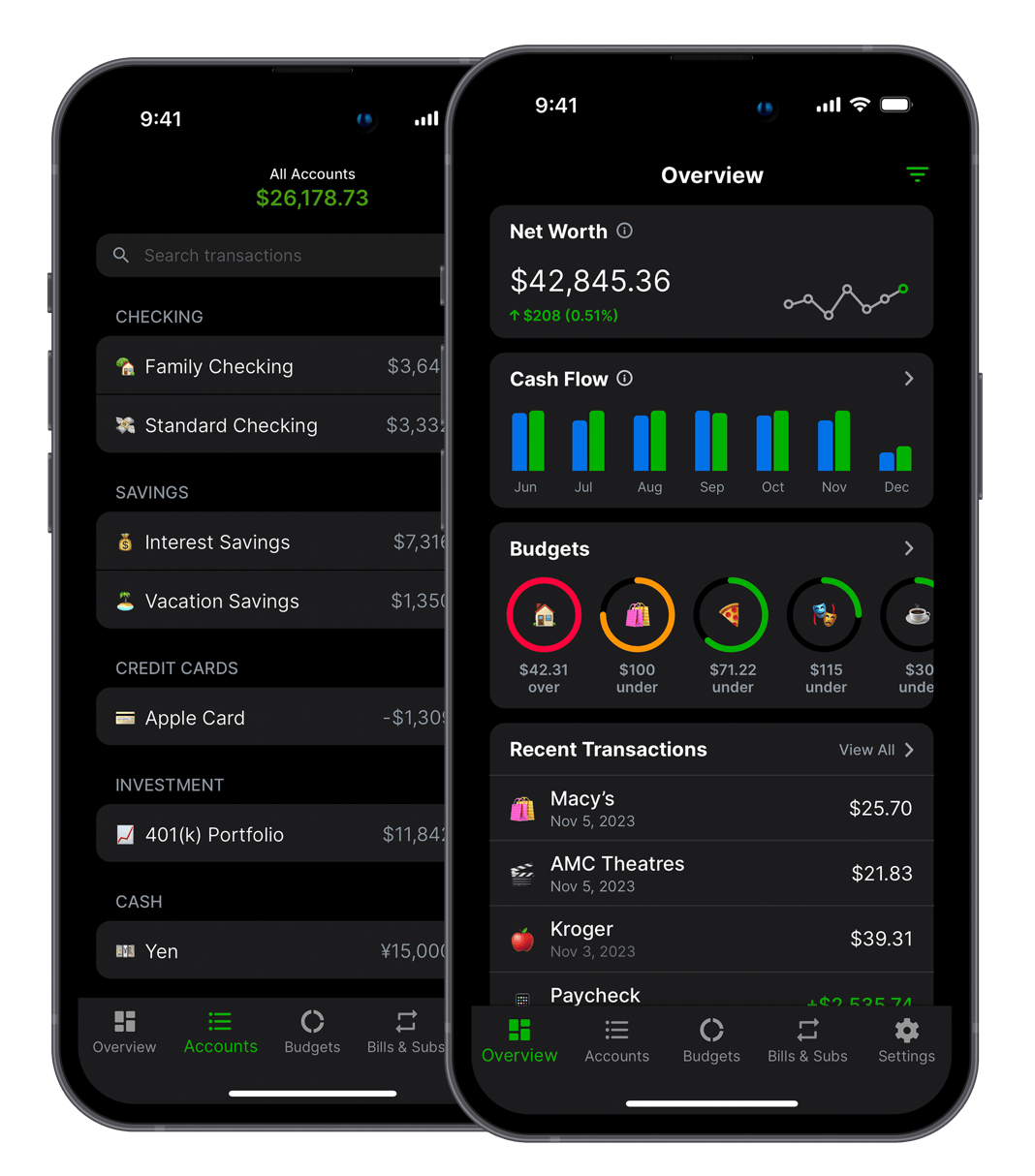

The reputation it built during that period is mostly earned. Monarch's budgeting section is genuinely thoughtful. You can set budget limits by category, roll unspent amounts forward to the following month (a feature that many users specifically missed from Mint), track progress toward savings goals, and view a clean summary of income versus spending for any period. The cash flow reports are among the clearest in the category, and the transaction categorization learns over time and gets meaningfully accurate after a few weeks of corrections.

The feature that most distinguishes Monarch from the alternatives is collaborative budgeting. Monarch was designed from the beginning to support shared finances for couples: both partners can connect their accounts, see shared budgets, and update transactions from separate devices, with everything synced in real time. Mint handled this situation poorly. Monarch handles it better than any other app in this comparison. If you're managing household finances with a partner and want a single system you're both actively using, Monarch is the most mature solution available.

Bank sync is reliable. The app connects through Plaid, covers the major US financial institutions, and in most cases doesn't require re-authentication every few weeks the way some competitors do. The mobile apps (iOS and Android are both supported) are polished and fast. The web app works but feels like the less-developed part of the product, which I've heard echoed by users who primarily manage finances from a laptop rather than a phone.

Here's where the recommendation gets complicated: the price. Monarch costs $14.99 a month or $99.99 a year. That puts it at the top of the personal finance app category. For a product that replaced something users were getting for free, $99.99/year is a meaningful ask, and the question of whether the feature set justifies it depends on which features you actually use.

For a couple who will both actively engage with the collaborative budgeting features, the value proposition is reasonable. You're paying roughly $8 per person per month for a shared financial operating system, which is defensible if you're using it properly. For a solo user who primarily wants transaction tracking, spending categories, and a monthly cash flow view, the honest answer is that Monarch's core functionality at this price point is hard to justify over less expensive alternatives that deliver 80 to 90 percent of the same capability.

The pattern I've observed among users who left Monarch: they stayed for two to three months, used the budgeting features actively in the first few weeks, and then drifted into using it primarily as a transaction ledger without engaging the goal-tracking or collaborative features that justify the price. At that point, the math stopped making sense, and they started looking for something cheaper that did the same thing.

Monarch is a good app. The question isn't whether it's good. The question is whether it's $99.99/year better than the alternatives for your specific situation, and for a majority of solo Mint refugees, the honest answer is no.

YNAB: the most effective system for people who will actually use it

YNAB has been around since 2004 and has built the most committed user community of any personal finance app. There are subreddits, YouTube channels, and podcast episodes dedicated entirely to YNAB methodology. Users who adopt it successfully tend to stay for years. People who stick with YNAB tend to be more financially engaged than users of any other tool in this category, and that correlation is not a coincidence.

The philosophy behind YNAB is called zero-based budgeting: every dollar you currently have in your accounts is assigned to a specific job before you spend it. You're not creating a budget based on projected future income. You're budgeting with the money you actually have right now. If you have $2,400 in your checking account today, you allocate all $2,400 across your categories (rent, groceries, gas, restaurant, emergency fund, and so on) until you reach zero. When more money comes in, you allocate that too.

This approach is philosophically different from how Mint worked. Mint was reactive: it categorized what you spent after the fact and showed you whether you stayed within your limits. YNAB is proactive: it asks you to decide what money is for before you spend it. The behavioral difference is significant. YNAB users who follow the system consistently report that it changes how they think about purchases in real time, not just in retrospect.

The four rules YNAB teaches are worth understanding even if you don't use the app:

- Give every dollar a job. Assign every dollar you have to a category before you spend it. No unallocated money sitting in checking.

- Embrace your true expenses. Annual and irregular expenses (car insurance, holiday gifts, dentist bills) should be broken into monthly amounts and funded a little at a time so they don't feel like surprises.

- Roll with the punches. When you overspend in a category, you don't fail. You move money from another category to cover it. The budget is a living document, not a judgment.

- Age your money. Over time, you want to be spending money that came in weeks ago rather than money that arrived this morning. This is a proxy for financial cushion and reduces paycheck-to-paycheck stress.

That framework is genuinely good financial thinking. Users who internalize it tend to build savings faster, carry less credit card debt, and have clearer pictures of their financial situations than people who track passively. The YNAB community's enthusiasm is not irrational.

The limitation is execution cost. Running YNAB as the system is designed requires active engagement every week, sometimes multiple times per week. You categorize transactions as they happen (or at minimum review them daily), reconcile accounts, move money between categories when plans change, and reflect on whether your category allocations still match your actual priorities. For users who are willing to invest that time, the return is high. For users who want their finances managed passively, YNAB will feel like a part-time job within six weeks, and they will quit.

The quit rate for YNAB is the worst-kept secret in the personal finance app space. The company doesn't publish data on it, but the pattern is visible in the forums: enormous enthusiasm in the first month, a lot of "I fell off the wagon" posts in month two, and a subset of highly committed users who become the vocal community that makes the product look more universally successful than it is.

If you want YNAB to work, you need to be honest with yourself about whether you're the kind of person who will open a budgeting app multiple times per week and actively manage categories. If the answer is yes, YNAB is probably the most powerful tool in this comparison. If the answer is "I'll try to be," the evidence suggests you should pick something that works with less maintenance.

The price is $109/year. Given the time investment required to use it correctly, I'd frame it as: you're paying $109/year for a system, not just software. If you're not committed to the system, you're paying $109/year for something you'll barely use.

If you're not sure which budgeting method fits how you actually manage money, it's worth working that out before committing to any app. I wrote a guide that walks through the options: which budgeting method is right for you.

Rocket Money: excellent at one specific job, not the job you probably need

Rocket Money's origin story matters for understanding what it actually is. The company launched in 2016 as Truebill, a service built around one specific problem: people had subscriptions they'd forgotten about that were quietly draining money from their accounts every month. Truebill would scan your bank transactions, identify recurring charges, and offer to cancel the ones you didn't want. It was good at this and built a real business around it.

Rocket Companies (the parent of Rocket Mortgage) acquired Truebill in 2021 for $1.275 billion and rebranded it as Rocket Money. The mandate became broader: build it into a full personal finance platform. The subscription-cancellation capability was retained as the flagship feature, and additional budgeting and tracking functionality was layered on top.

The subscription audit is still the app's strongest feature. Rocket Money surfaces recurring charges clearly, categorizes them, flags unusual billing amounts, and offers to negotiate or cancel services on your behalf (for a fee or a percentage of negotiated savings, depending on which tier you're on). For anyone who has ever discovered a $14.99/month charge from a trial they forgot to cancel six months ago, this is genuinely useful, and it's not a feature that Monarch, YNAB, or Copilot replicate as well.

The budgeting features are where Rocket Money shows its seams. They're functional but they feel grafted onto a product that was originally designed for a different purpose. Budget categories exist, spending summaries are available, and bank sync pulls transactions automatically. But the experience of building and maintaining a budget in Rocket Money is noticeably thinner than Monarch or YNAB, and the app's priority is clearly the subscription and bill-negotiation features rather than the day-to-day budgeting workflow.

The pricing structure deserves specific attention because it's deliberately confusing. Rocket Money offers a free tier with basic transaction viewing and limited budgeting. The Premium tier is presented with a range of $6.99 to $12.99 per month, and when you go to subscribe, the app presents you with a slider to choose your own price within that range. This is a pricing dark pattern: the anchor of $12.99 makes the lower amounts feel like a discount, but the app still costs money and the price you pay depends partly on how much you're willing to push back during checkout. Users who are aware of this and select the lower end pay less. Users who don't notice pay the maximum.

I've heard this framing from multiple Rocket Money users, and it's consistent with documented reports online: the pricing interaction makes the app feel adversarial. A personal finance tool should not make you feel like you're negotiating against it before you've even started using it. That feeling tends to color the entire experience.

Rocket Money is worth using if you have a genuine subscription audit problem and want a tool that will surface those charges, organize them, and help you cancel the ones you don't need. As a primary Mint replacement for someone who wants to track spending and maintain a budget, there are better options.

Copilot: the best product in the category, for a specific audience

Copilot is the app that most consistently earns the descriptor "beautiful" in user reviews, press coverage, and forum discussions. That reputation is accurate and somewhat undersells it. The design isn't just visually polished, it's functionally considered in a way that makes the experience of managing money feel less unpleasant than most financial apps manage.

The transaction categorization uses machine learning that gets genuinely smart over time. Copilot learns your merchants, applies consistent categories, and over the first few weeks of use, reaches a level of accuracy that minimizes the manual correction burden significantly. Investment account tracking is more sophisticated than what Mint offered, and more integrated into the overall financial picture than Monarch or YNAB attempt.

The AI-assisted insights are worth highlighting because they're more useful in practice than similar features in competing apps. Rather than showing you that you spent more on restaurants than your budget allowed (which all the apps do), Copilot identifies patterns: your grocery spending tends to spike in the third week of the month, or your utility bills have crept up 22 percent over the past six months. These observations take the data and do something interpretive with it rather than just displaying it.

The interface is designed for active financial management without the all-in commitment YNAB requires. You can set spending targets, review transactions in a swipe-based interface that makes categorization fast, and get a clear picture of the month's cash flow without needing to do manual reconciliation. For iPhone users who want a better-than-Mint experience with less overhead than YNAB, Copilot is genuinely excellent.

The platform limitation is absolute and it's the correct reason to eliminate Copilot from consideration before reading another sentence about it. Copilot is iOS and Mac only. There is no Android app. There is no web browser interface outside the Mac desktop application. If you use an Android phone, you cannot use Copilot. If you use a Windows computer and want to review your finances at work, you cannot use Copilot from a browser. If your household has one iPhone user and one Android user and you want a shared financial tool, Copilot doesn't serve half of that household.

Android's share of the US smartphone market is roughly 44 percent, which means Copilot is unavailable to nearly half the population. For an app priced at $71.99 per year or more (pricing has varied over time), that restriction is a significant product decision, and the app's developer has been explicit that Android is not on the near-term roadmap.

If you're in the iOS-and-Mac ecosystem and you want the best personal finance app available regardless of price, Copilot is probably it. If you have any Android or cross-platform requirement, move on.

Side-by-side at a glance

The table above shows annual costs for the paid tiers of each app. Rocket Money's range reflects its choose-your-own-price Premium structure. Balance Pro's range covers Premium ($47.99/year, manual entry) and Ultra ($99.99/year, automatic bank sync via Plaid).

How to actually choose

The "best Mint alternative" question doesn't have a single correct answer, and any article that tells you it does is optimizing for clicks rather than accuracy. What it has is a decision framework, and the first question in that framework cuts the field significantly.

How actively do you want to manage your budget?

If your honest answer is that you want to assign every dollar a job and engage with your categories multiple times per week, YNAB is probably the right answer. The system works if you work the system, and the user community is a genuine resource. Accept the learning curve, commit to the weekly maintenance, and the $109 annual cost will likely pay for itself in changed financial behavior.

If your honest answer is that you want transactions to import automatically, categories to be applied without much manual intervention, and a monthly review to be enough, then YNAB will frustrate you and you should eliminate it. The remaining options are Monarch, Copilot (if you're iOS-only), and Balance Pro.

Are you on Android or do you need web browser access?

If yes, Copilot is eliminated. Your options are Monarch or Balance Pro (and Rocket Money if the subscription audit is specifically valuable to you).

Are you budgeting with a partner?

If yes, Monarch's collaborative features are the most mature in the category and make the $99.99/year easier to justify. Both partners connecting accounts, sharing categories, and seeing real-time updates on shared budgets is Monarch's clearest advantage over the alternatives.

If you're managing finances solo, the collaborative features don't apply to you, and the remaining value proposition for Monarch at $99.99/year is harder to defend against less expensive alternatives that deliver similar core functionality.

What's your actual budget for this?

If spending more than $50/year on personal finance software feels like a significant amount, Monarch, YNAB, Copilot, and the upper tier of Rocket Money are all above that threshold. Balance Pro Premium at $47.99/year is the option designed for someone who wants real budgeting without the category-leading price.

Where I landed, and why I'm telling you this

I've been building Balance Pro since 2014, which predates most of the apps in this comparison. I built it because I wanted a budgeting tool that worked across iOS, Android, and a browser, set real spending limits rather than just categorizing history, and didn't require a complex methodology to maintain. More than a decade of building it and watching how real users actually engage with personal finance software has shaped what it does.

Balance Pro Premium ($47.99/year) handles manual transaction entry, budget categories with real limits, savings goals, bill and subscription tracking, and receipt scanning through AI-powered OCR. It runs on iOS, Android, and the web, with data synced across all three. Balance Pro Ultra ($99.99/year) adds automatic bank account sync through Plaid for users who want transactions to import without manual entry.

I'm not going to tell you Balance Pro is objectively better than the alternatives, because it isn't in every dimension. Monarch's collaborative budgeting is more developed than ours. Copilot's design is more polished. YNAB's zero-based methodology is more comprehensive if you're willing to put in the work. What I will tell you honestly, from years of watching how real users actually behave with personal finance apps, is that the features most people use consistently are the same features across all these apps: automatic transaction import, budget categories, and a monthly cash flow view. On those core features, the apps in this category are more similar than their marketing suggests. The meaningful differences are platform availability, price, and how much active management the system requires.

When someone comes to me now and asks which Mint alternative I recommend, I ask them the three questions in the section above: how actively do you want to manage, what devices do you use, and are you budgeting with a partner. Those three answers almost always narrow it down to one or two options, and the right answer is usually clear from there.

For the majority of solo Mint refugees on mixed-platform households who want something that works without significant ongoing maintenance and costs less than a monthly streaming subscription, the answer that comes up most often is not Monarch Money. That's the honest version.

Frequently Asked Questions

Is Monarch Money worth the price?

Monarch Money is well-designed with solid budgeting features, but at $99.99 per year it's the most expensive option in the personal finance app category. The value proposition is strongest for couples using the collaborative budgeting features. For solo users who primarily want transaction tracking and basic spending categories, less expensive alternatives deliver comparable core functionality.

What's the best free Mint alternative?

None of the top Mint alternatives offer a genuinely useful free tier comparable to what Mint provided. Monarch Money, YNAB, and Copilot are all paid apps. Rocket Money has a free tier limited to basic transaction viewing without real budgeting. Mint's free model was subsidized by credit card and loan referrals. That model has largely disappeared from the category, and the honest answer is that useful budgeting software now costs money.

How is YNAB different from Monarch Money?

YNAB uses zero-based budgeting: every dollar you have is assigned to a category before you spend it, which requires active weekly engagement. Monarch Money is passive: bank sync categorizes transactions automatically and you review after the fact. YNAB changes financial behavior more deeply for users who commit to the system. Monarch is easier to maintain for users who want automation over active management.

Does Copilot work on Android?

No. Copilot is iOS and Mac only. There is no Android app and no web browser access outside the Mac desktop app. If you use an Android phone or primarily work from a Windows computer, Copilot is unavailable to you entirely. This is the most significant limitation of an otherwise well-regarded app, and the developer has not announced Android support on any near-term roadmap.

What's the best Mint replacement that works on both iOS and Android?

Monarch Money and YNAB both support iOS and Android. Balance Pro runs on iOS, Android, and web. Copilot is iOS and Mac only. Rocket Money supports iOS and Android but has limited budgeting features. If cross-platform access is a requirement, your real choice is Monarch Money ($99.99/year), YNAB ($109/year), or Balance Pro ($47.99/year for Premium, $99.99/year for Ultra with automatic bank sync).

Why did Mint shut down?

Intuit shut down Mint in October 2023 and redirected users to Credit Karma, which Intuit also owns. The underlying cause was that Mint's free model, funded by credit card and financial product referrals, was no longer generating enough revenue to justify the infrastructure cost. Intuit also owns Credit Karma, which occupies a similar position with better monetization. The shutdown was a business decision, not a product failure.

What happened to Mint users after it shut down?

Mint had approximately 3.6 million active users at shutdown, most of whom were redirected to Credit Karma, which doesn't replicate Mint's budgeting features. The displaced users spread across Monarch Money, YNAB, Copilot, Rocket Money, and smaller alternatives. Monarch Money saw the largest single wave of new signups immediately following the announcement, partly because of targeted acquisition campaigns aimed at Mint users.