Key takeaways

- Most budgets fail because they're built on guesses. Track your real spending for 30 days first, then set limits from that data.

- The 50/30/20 framework (needs, wants, savings) is a starting point, not a prescription. Your actual numbers will tell you where to adjust.

- A five-minute weekly check-in does more for a budget than a monthly deep-dive you keep skipping.

- Going over in a category isn't failure. It means your estimate was wrong. Adjust the number and keep going.

- You don't need willpower. You need a system with low enough friction that you'll still be using it in September.

I've been building Balance Pro since 2014, which means I've spent more than a decade watching how people actually manage their money, not how they plan to. The pattern I see most often isn't someone who tried to budget and failed because they weren't disciplined enough. It's someone who built a budget before they knew what their spending actually looked like, hit a wall in week two, and concluded the whole thing wasn't for them.

The conclusion was wrong, and so was the system. There's a difference, and it matters, because the right system for most people isn't more complicated than what they already tried. It's just built in a different order.

Why do most budgets fail in the first month?

The failure mode is almost always the same. Someone decides to start budgeting, opens an app or a spreadsheet, and starts typing limits. $500 for groceries. $200 for dining out. $150 for subscriptions. These numbers come from a rough intuition about what sounds responsible: maybe an article they read once, maybe a calculator that suggested 50/30/20 without knowing anything about their actual life.

Then the first real month happens. The grocery number was $300 underestimated. Dining out was double what they budgeted. A dentist appointment showed up, a car registration, and three Amazon charges they'd completely forgotten about. The budget looks like it detonated, they feel like they failed at something everyone else seems to have figured out, and the app goes unused for the next three months.

None of that was a discipline problem. The budget failed because it was built on guesses. The fix is to reverse the order: track first, budget second.

Step 1: Should you track your spending before setting any limits?

Yes, and this is the single most important thing in this entire guide. Before you set a single budget target, spend 30 days watching your money without any rules or judgment. No limits, no "I should spend less on this." Just data.

This feels passive, but it's the most productive thing you can do in month one. At the end of it, you'll know your actual grocery number, not your hoped-for one. You'll see the annual subscriptions that hit once a year and always feel like a surprise. You'll find the apps you're paying for that you haven't opened since last year. You'll notice the dentist bill, the quarterly insurance premium, and the "one-time" purchase that somehow shows up every few months.

You cannot build a realistic budget without this information. Any targets you set before you have it are guesses, and we've already established what happens to budgets built on guesses.

Balance Pro handles the tracking automatically once you connect your accounts. Transactions import from your bank and credit cards, get sorted into categories, and show up without any data entry on your end. If you'd rather not connect accounts, manual entry works fine too. Either way, by day 30, you have a real picture of where your money goes. The first month of data is almost never what people expect: most people underestimate their dining spend by 30 to 50 percent and forget about recurring charges almost entirely. Seeing the real numbers isn't a verdict on your habits. It's just the starting point.

Step 2: How do you sort spending into categories that actually make sense?

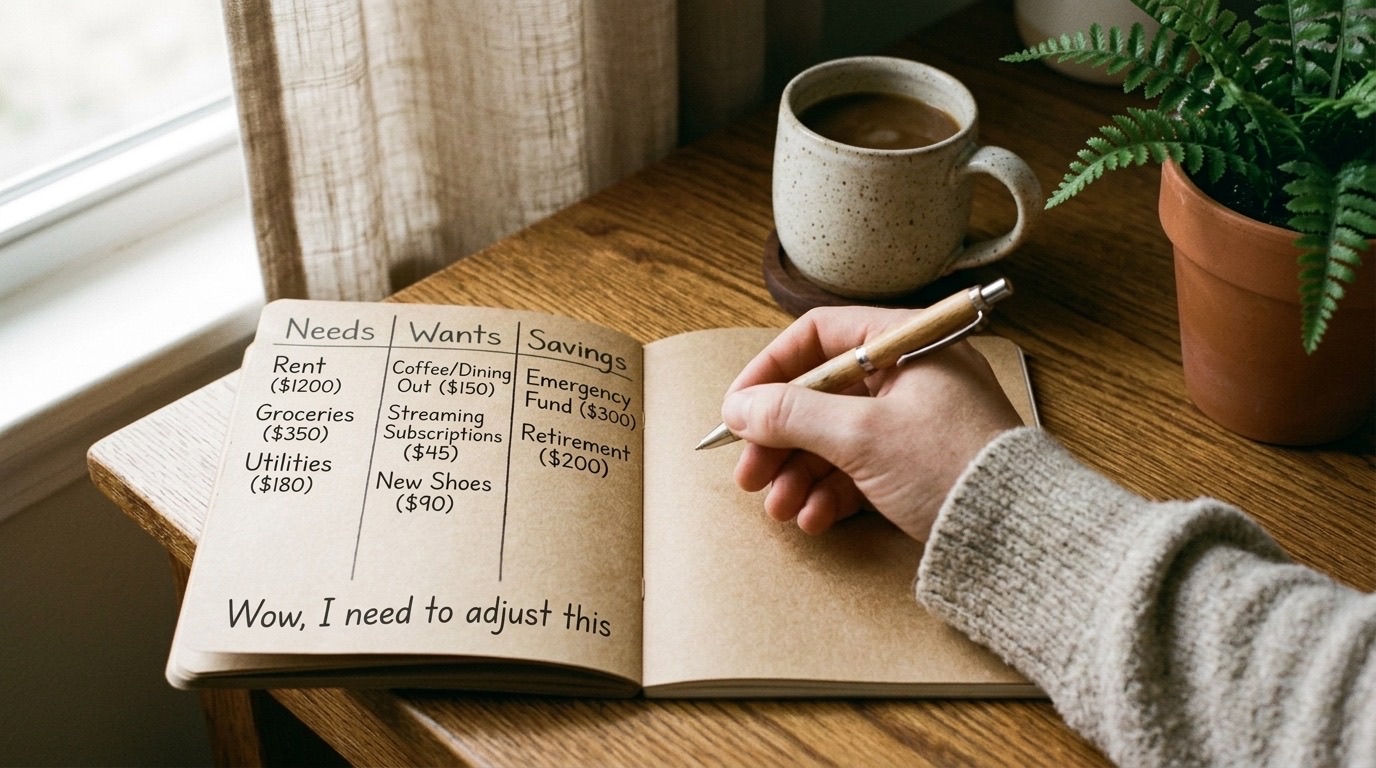

Once you have 30 days of data, the next step is to make sense of it. The framework I'd start with is 50/30/20: roughly 50 percent of your take-home pay to needs, 30 percent to wants, and 20 percent to savings and debt repayment.

Needs are the non-negotiables: rent or mortgage, groceries, utilities, insurance, minimum debt payments, and transportation to work. If you genuinely couldn't function without it, it's a need.

Wants are everything you could technically live without, even if you'd rather not. Dining out, streaming services, the gym membership, concerts, that coffee habit, the clothing purchases that weren't replacing something worn out. These aren't bad expenses. They're just discretionary.

Savings and debt payoff is any money you're setting aside: a 401(k) contribution, an emergency fund, paying down debt faster than the minimum. Treat this as a non-optional line item, not whatever happens to be left at the end of the month.

The 50/30/20 split is a lens, not a law. If you live in a high cost-of-living city, your needs category will almost certainly be over 50 percent of take-home pay, and that's not a personal failing. It's just math. The value of the framework is that it gives you a structure for categorizing what you see, and for spotting where things feel out of proportion.

When I look at a first month of data, the most common finding is that the needs bucket is roughly fine, the savings bucket is lower than the person would like, and the wants bucket has a few surprises: usually some forgotten subscriptions, and dining out that added up faster than it felt like it should have. That's useful information. That's what you build from.

Step 3: How do you set budget targets that are actually realistic?

Here is where most budgeting advice goes wrong. It tells you that a "healthy" grocery budget is $300 a month for a single person, or that dining out should stay under 15 percent of income, or that you should automatically save 20 percent starting now. These numbers are averages built from aggregate data that has nothing to do with how you actually live, where you live, what you eat, or what your income actually is.

Your budget targets should come from your actual spending data, with a realistic adjustment layer on top.

If you spent $680 on groceries last month, your grocery budget doesn't start at $400 because some article said so. It starts at $680. Maybe you look at that and decide you want to bring it to $620, and you have a specific plan: batch cooking on Sundays, fewer specialty items, one fewer delivery order a week. That's a target. A number you invented because it sounded responsible is not a target. It's a wish.

The same logic applies to every category. Look at what you actually spent, decide if that's where you want to be, and set a target that reflects both reality and intention. The first time you build a budget this way, it will feel less flattering than one built on aspirations. It will also survive contact with an actual month.

| Category | Budget built on guesses | Budget built on data |

|---|---|---|

| Groceries | $300 (sounds responsible) | $640 (what you actually spent) |

| Dining out | $150 (aspirational) | $380 (real number, target adjusted to $320) |

| Subscriptions | $50 (rough guess) | $127 (found four forgotten services) |

| Irregular expenses | $0 (forgot to account for them) | $180 (dentist, car registration, annual fees) |

| Result | Blown by week two, abandoned by week three | Uncomfortable at first, workable by month two |

The data-driven budget isn't prettier. It might be more sobering to look at initially, because it shows you what's real instead of what you hoped for. But a realistic budget you maintain is worth dramatically more than an aspirational one you abandon in the first month.

Step 4: What does a five-minute weekly check-in actually look like?

The part of budgeting that people most consistently skip is also the part that makes everything else work: a regular, short review. Not a monthly deep-dive, not a quarterly reconciliation. A five-minute check-in, once a week, on the same day.

My actual routine, which I run Monday mornings with coffee:

- Scan last week's transactions. Flag anything miscategorized or that I don't recognize. This takes about two minutes when transactions are already imported automatically.

- Check category progress for the month. Is anything already at 80 percent with two weeks left? That's the signal to pay attention, not to panic, but to notice.

- Note anything coming up that needs money set aside. A flight I booked, an annual subscription renewing, a birthday dinner planned for the following weekend.

- Close the app. Done until next Monday.

The whole thing takes five minutes because the transactions are already there. I'm not entering data or building formulas. I'm reading what happened and thinking briefly about the week ahead.

The weekly cadence matters because monthly is too slow. By the time a monthly review reveals that dining out ran 40 percent over budget, you're already five days into the next month and you've had brunch twice. Checking once a week keeps you ahead of problems instead of perpetually reacting to them after the fact.

If five minutes sounds too short to be meaningful, I'd push back on that framing. The goal isn't a comprehensive financial audit. It's a quick scan to catch anything that needs attention before it compounds. Most weeks there's nothing urgent. Occasionally you'll catch something worth adjusting early. The habit is what matters, and a five-minute habit is one you'll actually keep.

Step 5: When and how should you adjust your budget each month?

At the end of every month, before the new one starts, spend about 10 minutes looking at how the month actually went and updating your targets accordingly.

This is not admitting failure. This is how a budget is supposed to work.

A budget is a hypothesis about where your money will go. At the end of the month, you compare the hypothesis to what actually happened and update it. If your grocery budget was $620 and you spent $670 three months in a row, your grocery budget is $670. Adjust it. If dining out ran over every single month, either you need to change the behavior or you need to accept that dining out is a genuine priority and find another category to pull back. Both are valid choices. What isn't useful is keeping the same targets and feeling bad about missing them repeatedly.

A few things worth accounting for in monthly adjustments:

- Seasonal expenses. Utilities run higher in winter and summer. Holiday gifts cluster in November and December. Travel spending spikes in summer for most people. These aren't surprises after you've tracked for a year. Build them into the relevant months instead of letting them blow up your otherwise normal budget.

- Annual and quarterly charges. Car registration, insurance premiums, software subscriptions, professional memberships. Balance Pro flags recurring transactions, so they're easy to spot and plan around well before they hit.

- Life changes. New job, new apartment, new kid, new car payment. Each of these changes the inputs to your budget, and the budget should reflect the life you're actually living, not the one you were living six months ago.

The goal isn't a budget that never changes. It's a budget process that adapts as your life does, and that stays close enough to reality that you'll keep using it.

What do you do when you go over budget?

Adjust the number and keep going.

Going over in a category means your estimate was wrong, not that you failed at something. The most common reason people abandon their budgets is a single month of overages that makes the whole thing feel pointless. It's a terrible conclusion to draw from what is essentially a math error.

If you went over, you have information you didn't have before. Either the target was unrealistic and needs to go up, or something specific happened that month and the target was actually fine. Both are worth knowing. A dentist bill in a month where you went over on healthcare isn't a budgeting failure. It's an argument for building a small irregular expenses buffer into your monthly plan.

The people I know who've maintained a budget for years are not the ones who never overspend. They're the ones who overspend, look at what happened, update the number, and keep the month going without treating it as a moral verdict. A budget you've been using for eight months with occasional imperfect weeks is worth more than a perfect system you rebuilt three times and never actually maintained.

A budget you've been using imperfectly for eight months is worth more than the perfect one you abandoned in February.

Getting started with Balance Pro

If you want to run this system without the manual tracking overhead, Balance Pro handles the data layer automatically. Connect your accounts once, and transactions import, get categorized, and show up ready for your weekly review. You can set budget targets for each category, watch progress through the month, and get the snapshot you need in about five minutes. Premium is $47.99 a year and includes budgets, goals, custom categories, and CSV export. Ultra is $99.99 a year and adds automatic bank sync and AI receipt scanning.

Manual entry works just as well if you'd prefer to keep your accounts private. Either way, the system is the same: track for 30 days, sort what you see into needs, wants, and savings, set targets from real numbers, do a five-minute check-in each week, and adjust at the end of every month. That's the whole thing. It doesn't require a financial background or a complicated setup. It just has to be done in the right order.

Frequently Asked Questions

How do I make a budget from scratch?

Track your spending for 30 days without setting any limits. Use that real data to set category targets. Sort your spending into needs, wants, and savings using the 50/30/20 framework as a starting point. Then run a five-minute weekly check-in and adjust your targets each month as your life changes. The order matters: track first, budget second.

What is the 50/30/20 rule and does it actually work?

The 50/30/20 rule allocates 50 percent of take-home pay to needs, 30 percent to wants, and 20 percent to savings and debt repayment. It works as a starting framework, not a law. In high cost-of-living areas, needs often push past 50 percent, and that's fine. The value is in using the categories to understand where money goes, not in hitting a specific ratio.

How often should I review my budget?

Weekly for a quick five-minute transaction scan, and monthly for a broader review of category targets. The weekly cadence keeps you current and lets you catch overspending before it compounds. Monthly is when you update targets based on what actually happened and account for what's coming in the next month.

What should I do if I go over budget in a category?

Adjust the target and keep going. Going over means your estimate was wrong, not that the system failed. Either revise the target upward to match reality or make a specific change to reduce the spending. A budget you've maintained for six months with occasional overages is worth far more than a perfect one you abandoned in February.

What is the best budgeting app for beginners?

Balance Pro is built for exactly this. It imports transactions automatically, categorizes them, and shows spending by category without a complicated setup. Premium is $47.99 a year and covers manual tracking, custom categories, budgets, and goals. Ultra is $99.99 a year and adds automatic bank sync. Most people are up and tracking within 15 minutes of signing up.

The "track for 30 days first" advice in step one isn't theoretical. A friend let me walk through what happens when you actually do this for six months in I tracked every dollar for 6 months: here's what changed, with specific dollar amounts and the patterns that showed up.